Risk Models For Banks. This tutorial outlines several free publicly available datasets which can be used for credit risk modeling. Banks have continued with the widespread use of analytical models, attracting constant attention on how best to measure.

The risk model can be used to review your portfolio's historical performance and to assess what fraction of the returns come from common.

The calculations have been done by using SPSS and MATLAB software.

Risk Management Framework - Commercial Bank Sri Lanka

Terence Ng Tsz Wang - Head, Model Risk Management ...

Graph Theory for Systemic Risk Models

Model Risk Management for Banks and non-Banks - YouTube

Credit Risk - Modeling - Enterprise Services WIKI - SCN Wiki

Corporate Banking Snippets - Risk Models - Risk Funnel ...

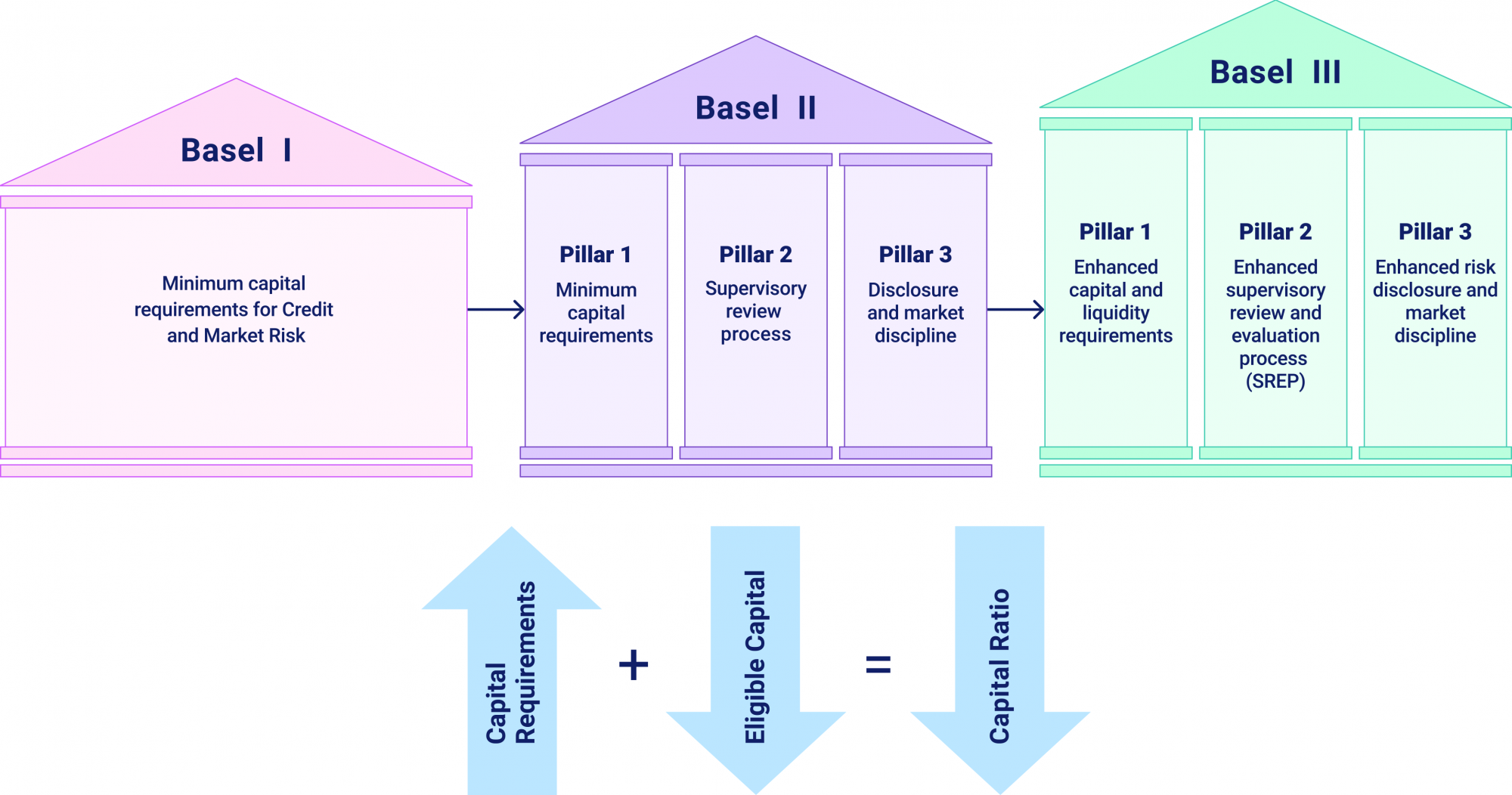

Towards better Risk Management..Basel III – Vamsi Talks Tech

BSA/AML Compliance - MBAF, CPAs and Advisors

Banks look to repurpose credit risk models for IFRS 9 ...

Effective Internal Risk Models for FRTB Compliance: The ...

Datencenter-Strukturen-des-Risikomanagements

Data Science In Banking: 7 Major Applications - Fireblaze ...

Report Credit Risk Models for Managing Bank’s Agricultural ...

SR 11-07 Compliance in Model Risk Management

Credit risk models in banks pdf

Jochen Theis - Head, Market Risk Models @ Standard ...

Credit risk models in banks pdf

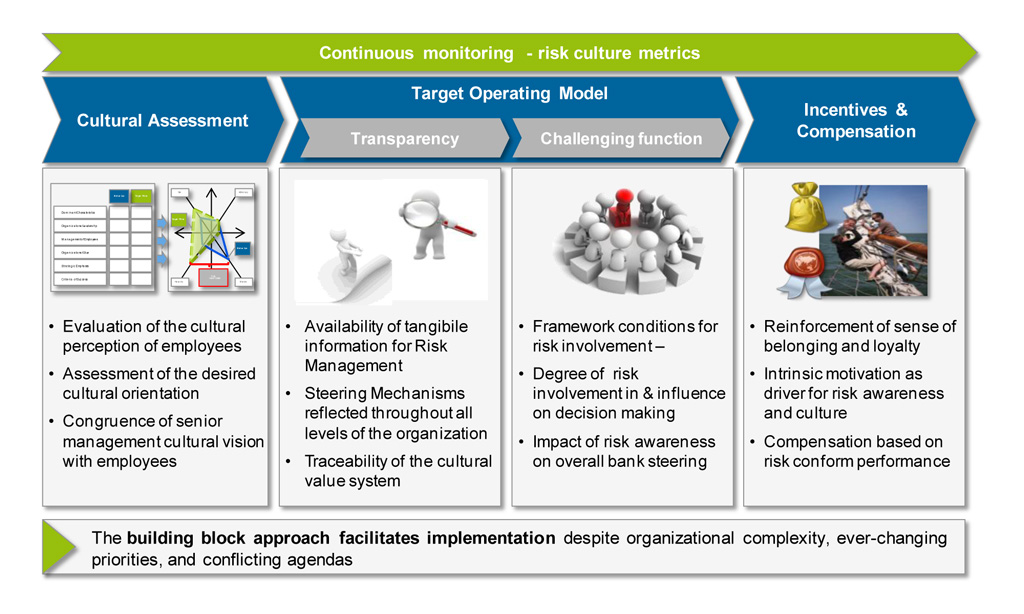

No comprehensive risk management without risk culture ...

(PDF) Testing backtesting : an evaluation of the Basle ...

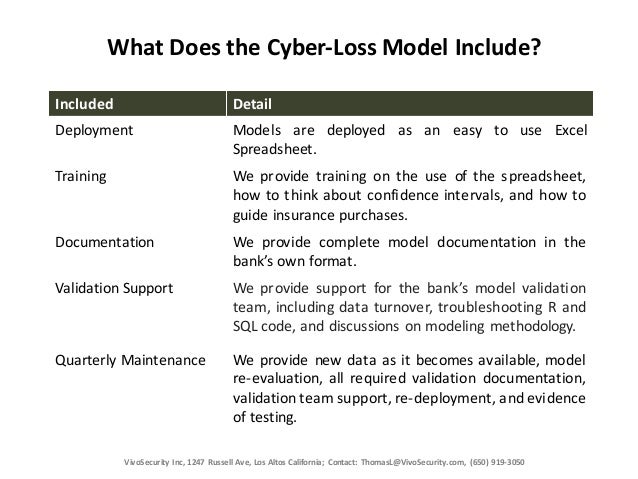

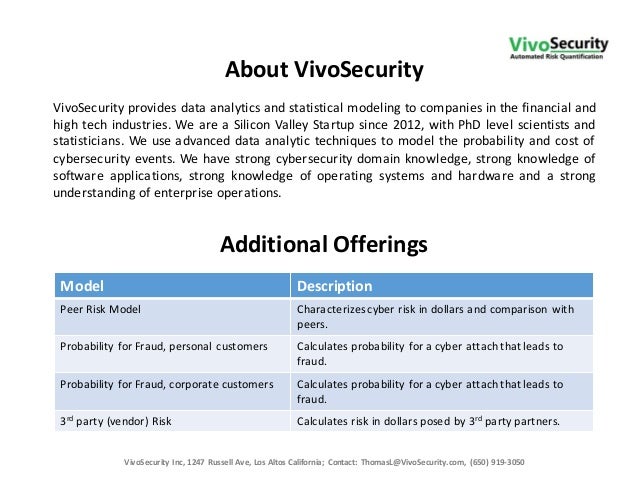

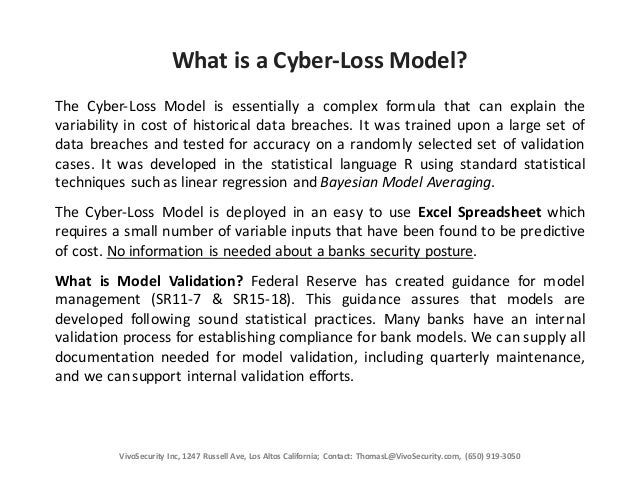

Cyber Op Risk Model, banks v7p4

Credit risk models in banks pdf

7 Key Drivers Of Credit Risk In Commercial Loan Portfolios ...

A new multi-factor risk model to evaluate funding ...

Report Credit Risk Models for Managing Bank’s Agricultural ...

Business — Banking — Management — Marketing & Sales » Risk ...

Credit risk models in banks pdf

Cyber Op Risk Model, banks v7p4

Cyber Op Risk Model, banks v7p4

CYBG joins the big British banks' risk model club ahead of ...

7 Key Drivers Of Credit Risk In Commercial Loan Portfolios ...

Operational-Risk Costs High for Banks and Challenging the ...

Future of Banking (Year 2025) - Banking Technologies, Risk ...

ECB to Review Banks’ Risk Models for Next Three Years

Graph Theory for Systemic Risk Models

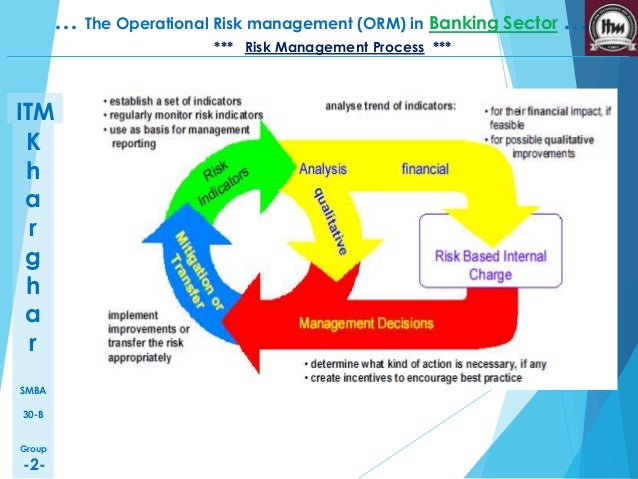

Operation Risk Management in Banking Sector

Group's risk management mission | Bank Millennium

Advanced Analytics |Maximize Your ROI via Predictive ...

Banks warned off machine learning for model risk - Risk.net

Model Risk Management (MRM) | Deloitte Deutschland

Credit risk models in banks pdf

New guidance on Model Risk - Manage your bank, not your model

Fintech | Lynx-BPM

Best Model Risk Management Practices for Banks

With SAS(R) Model Risk Management, Banks Gain Clarity on ...

What are widely used underwriting models in credit risk ...

Demand for Candidates with Risk Management Skills in Hong ...

(PDF) The use of portfolio credit risk models in Central Banks

What is a risk model? | SAS

Donald R. van Deventer's Blog - An Introduction to Credit ...

Report Credit Risk Models for Managing Bank’s Agricultural ...

Credit risk models in banks pdf

Cyber Op Risk Model, banks v7p4

Bank cyber chiefs at odds over risk models - Risk.net

SAP, Oracle Scrambling For GRC Dollars - CBS News

Best Model Risk Management Practices for Banks

Credit risk models in banks pdf

Quantification and management of model risks against the ...

Risk Management_269 – IRMT

Model Risk Management in U.S. Regional Banks

Basel IV to ban banks’ own risk models

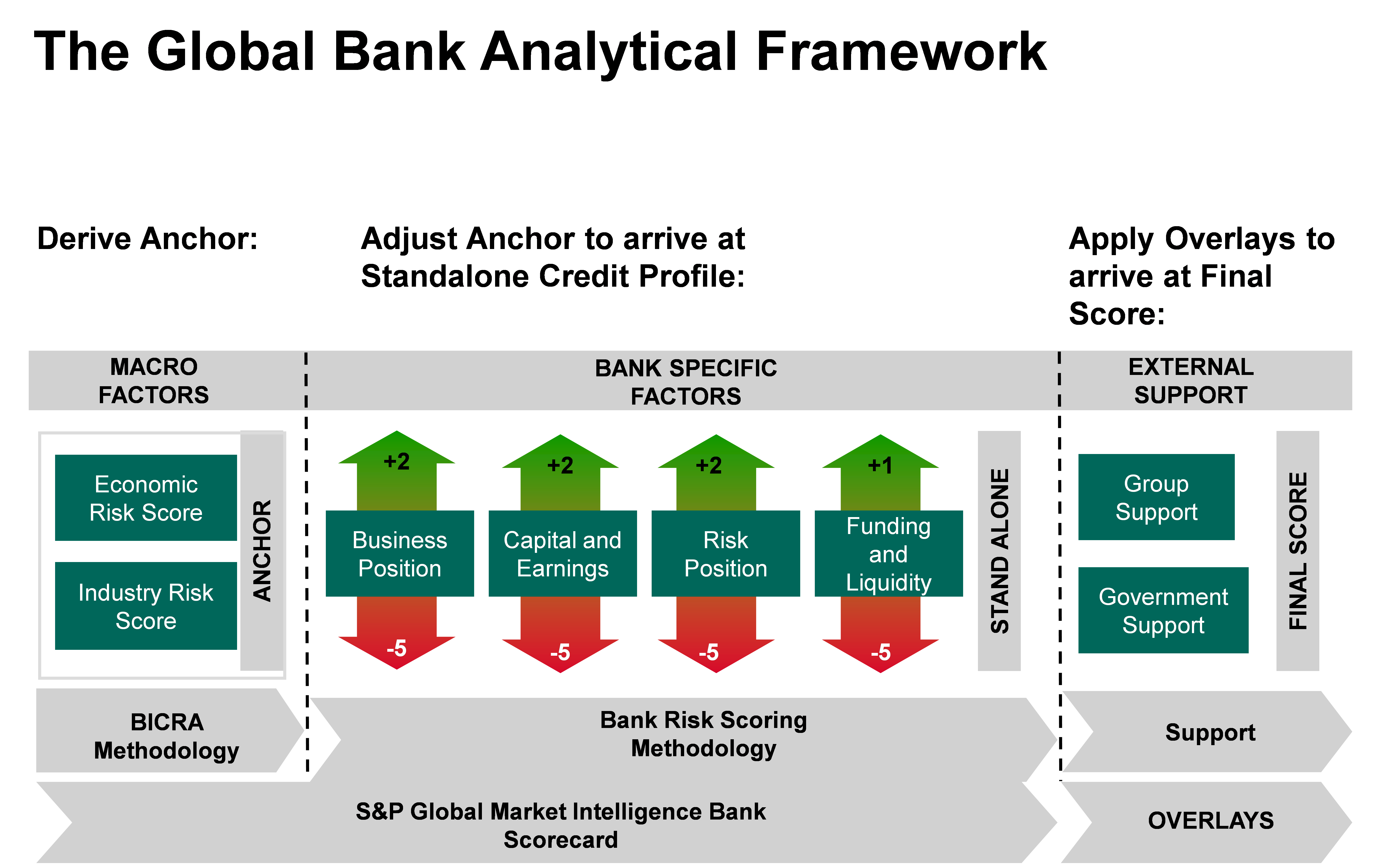

Banking risk management responsibilities expand far beyond the area of limiting credit risks and implementing procedures to monitor those risks. The bank applies the Value at Risk (VAR) models for measuring the trade and the bank portfolios' market risk and for the potential losses assessment via an appropriate analytical method supported by empirical circumstances and documented analysis. They are used to quantify credit risk at counterparty or transaction level in the different phases of the credit cycle (e.g. application, behavioural, collection models).